Pricing vulnerable options under a stochastic volatility model |

| |

| Affiliation: | 1. Department of Mathematics, Yonsei University, Seoul 120-749, Republic of Korea;2. Department of Mathematics, Sungkyunkwan University, Suwon, Gyeonggi-do 440-749, Republic of Korea |

| |

| Abstract: |

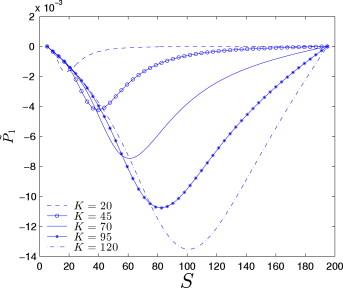

In this paper, we consider the pricing of vulnerable options when the underlying asset follows a stochastic volatility model. We use multiscale asymptotic analysis to derive an analytic approximation formula for the price of the vulnerable options and study the stochastic volatility effect on the option price. A numerical experiment result is presented to demonstrate our findings graphically. |

| |

| Keywords: | Vulnerable option Stochastic volatility Multiscale |

| 本文献已被 ScienceDirect 等数据库收录! |

|